Why Is It Important to Reconcile Your Bank Statements?

Bank statement reconciliation is a crucial financial practice that involves matching your bank statement transactions with your personal or business accounting records.

Note: reconciliation is usually done using XLS or CSV bank statements which are achievable using a bank statement converter if your default statements come as PDFs.

If you've ever wondered "What does it mean to reconcile a bank statement?" or "Why is it helpful to check each transaction on your statement?", this comprehensive guide will answer all your questions.

What Is Bank Statement Reconciliation?

Bank statement reconciliation is when you validate that all transactions from your bank statement match your records. This process involves carefully comparing each transaction in your bank statement against your personal or business financial records (such as purchase receipts) to ensure everything aligns correctly.

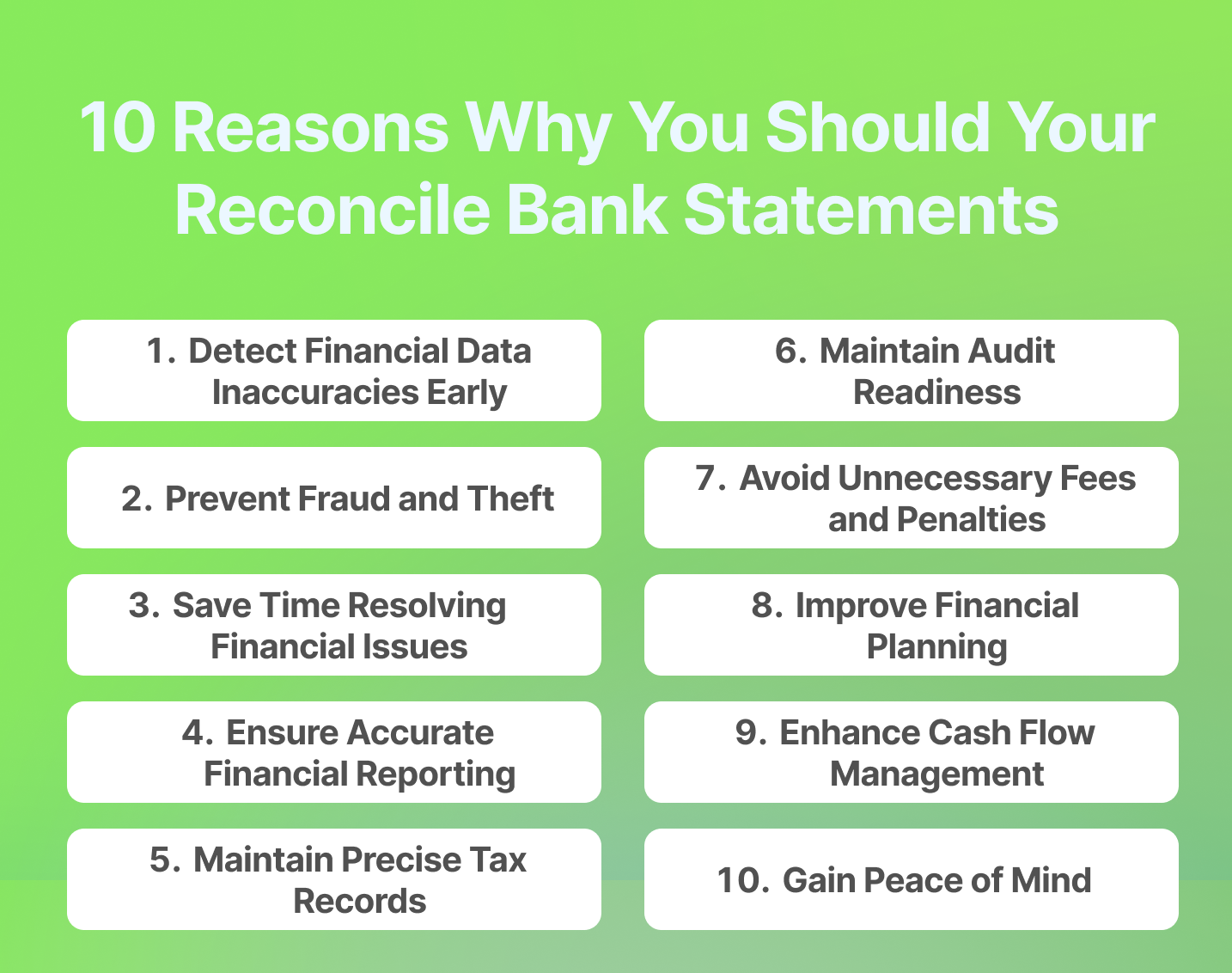

Why Is It Important to Reconcile Your Bank Statements? - 10 Critical Reasons

Understanding why it's important to reconcile your bank statements regularly can help you maintain better financial health and help the businesses you do accounting for get a better hold of their finances.

Here are 10 essential reasons for you to understand the importance of reconciling bank statements:

1. Detect Financial Data Inaccuracies Early

When you reconcile a bank statement regularly, you can quickly spot errors like double billings or missed payments. This early detection prevents small discrepancies from becoming major financial issues.

2. Prevent Fraud and Theft

By checking each transaction on your statement regularly, you can quickly identify unauthorized charges and potential fraud, allowing for immediate action.

Without a regular bank reconciliation, these issues can often go unnoticed, causing people and businesses losses of thousands of dollars.

3. Save Time Resolving Financial Issues

Addressing discrepancies promptly through regular reconciliation prevents the accumulation of complex financial problems that could take hours or days to resolve later.

4. Ensure Accurate Financial Reporting

I don't know about your experience with banks but let's just say banks aren't perfect and infallible. Regular reconciliation ensures your financial statements provide a true picture of your financial position. This accuracy is crucial for both personal budgeting and business decision-making.

5. Maintain Precise Tax Records

Regular bank statement reconciliation ensures accurate tax reporting. This precision helps avoid penalties and provides necessary documentation in case of audits.

6. Maintain Audit Readiness

Keeping reconciled records ensures you're always prepared for potential audits, whether for personal tax purposes or business requirements.

7. Avoid Unnecessary Fees and Penalties

Regular reconciliation helps catch potential overdrafts or account issues before they result in costly fees and penalties for you or the businesses you work for.

Without regularly downloading and checking bank statements, consumers and businesses are often unaware of these costs.

8. Improve Financial Planning

Understanding your true financial position through regular reconciliation enables better budgeting and financial planning decisions.

9. Enhance Cash Flow Management

Regular bank statement reconciliation provides clear insights into your cash flow patterns, helping you better understand how much money comes in and goes out and where you're spending/earning more.

10. Gain Peace of Mind

Last but not least, regular bank statement reconciliation provides confidence in your financial records' accuracy, allowing you to focus on other important aspects of your life or business.

Businesses without a clear view of their finances will always struggle to plan and execute mid to long-term, always living from month to month not knowing if they'll survive.

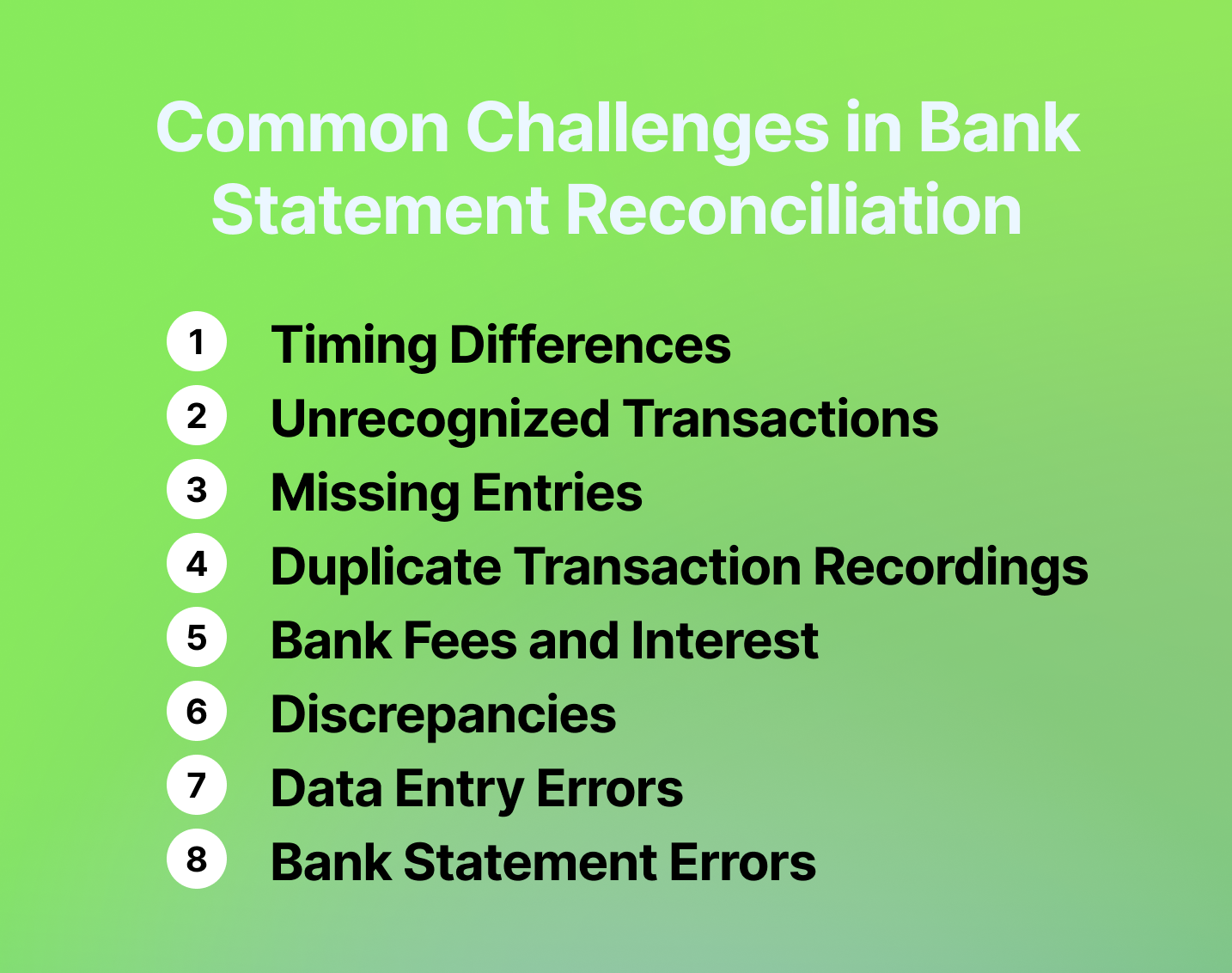

Common Challenges in Bank Statement Reconciliation

When reconciling your bank statements, you'll likely encounter several challenges that can complicate the process. Understanding these challenges helps you address them more effectively:

1. Timing Differences

Transactions might appear on your bank statement in a different period than when you recorded them. This is especially common with end-of-month transactions or automatic payments that process after business hours.

2. Unrecognized Transactions

You may find charges or deposits you don't immediately recognize. These could be recurring subscriptions, automated payments, or transactions using unfamiliar merchant names. Always investigate these thoroughly to prevent overlooking fraudulent charges.

3. Missing Entries

Some transactions might appear on your bank statement but be missing from your records. This often happens with:

- Automatic bank fees

- Direct debits you forgot to record

- Electronic transfers

- Interest payments or charges

4. Duplicate Transaction Recordings

Sometimes transactions get recorded twice in your accounting system, particularly when:

- Multiple people have access to the accounting system

- Manual entries are made alongside automated imports

- Backup records are merged incorrectly

5. Bank Fees and Interest Discrepancies

Banks may apply fees or interest charges that weren't anticipated in your records. These might include:

- Monthly maintenance fees

- Overdraft charges

- ATM fees

- Interest earned or charged

- Service charges

6. Data Entry Errors

Manual data entry can lead to various mistakes, such as:

- Transposed numbers

- Incorrect decimal point placement

- Wrong dates

- Misclassified transactions

7. Bank Statement Errors

While rare, banks can make mistakes. These might include:

- Double-posted transactions

- Missing transactions

- Incorrect amounts

- Transactions posted to the wrong accounts

Best Practices for Effective Bank Statement Reconciliation

Follow these key practices to ensure efficient and accurate bank statement reconciliation:

1. Set a Regular Schedule: reconcile your statements at least monthly, ideally at the same time each month. This consistency helps catch discrepancies early and maintains organized records.

2. Use Digital Tools: implement accounting software that automates the matching process. This reduces manual errors and saves significant time compared to paper-based reconciliation.

3. Document Everything: keep clear records of all transactions, including receipts and invoices. A good filing system makes it easier to investigate any discrepancies.

4. Act on Discrepancies Promptly: address any differences between your records and bank statements as soon as you spot them. Quick action prevents issues from snowballing.

5. Maintain a Backup System: keep copies of all reconciliation reports and supporting documents. This creates an audit trail and helps track historical changes.

6. Create a Checklist: follow a standardized reconciliation checklist to ensure you don't miss any steps in the process. This helps maintain consistency across all reconciliations.

7. Review Outstanding Items: keep track of checks and deposits that haven't cleared yet. This helps explain the differences between your records and bank balance.

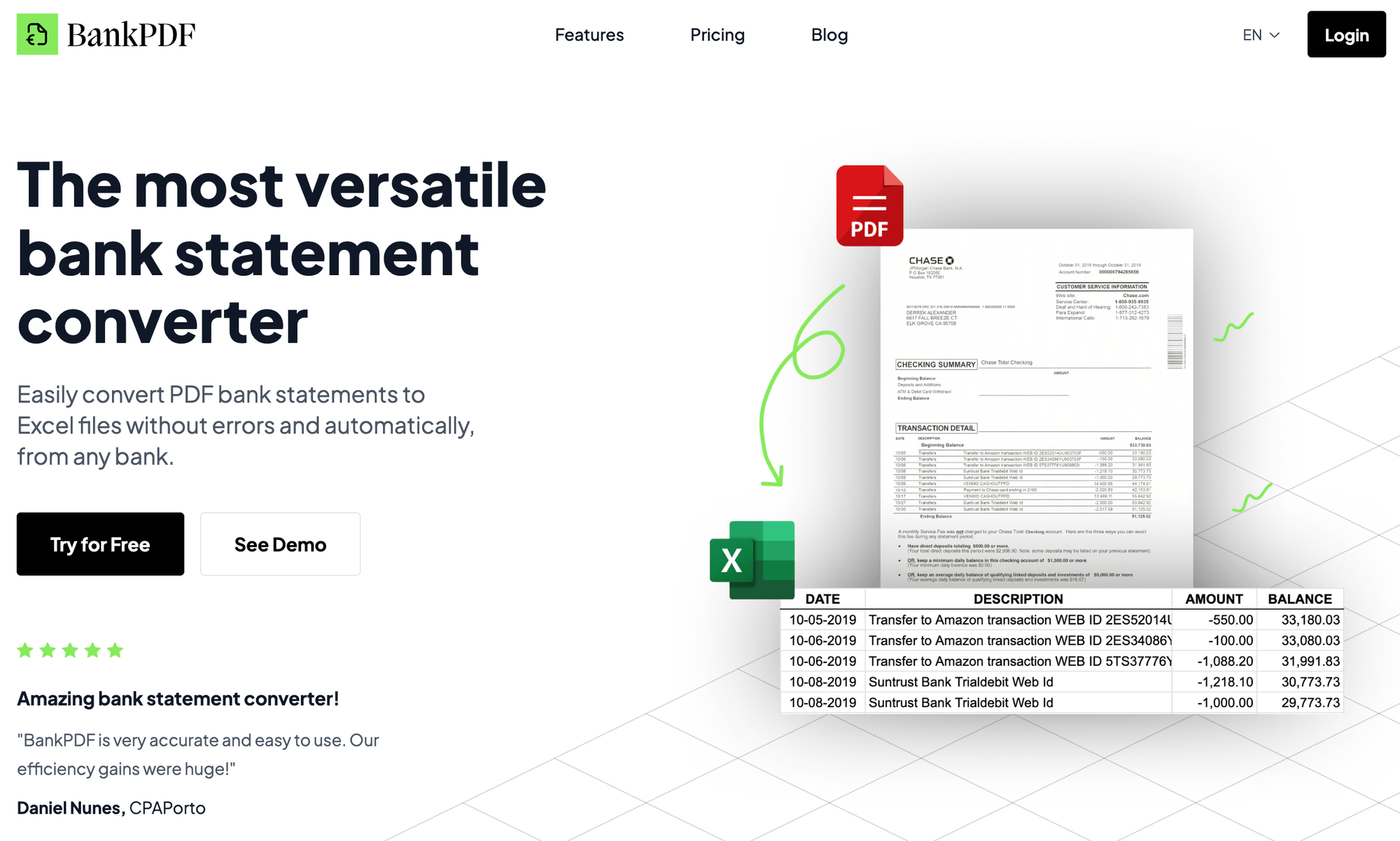

How BankPDF Can Help in Bank Statement Reconciliation

Whether you're managing personal finances or responsible for the accounting of a business, regular bank statement reconciliation helps ensure accuracy, prevent fraud, and maintain proper financial records.

However, managing so many bank statements and transactions can be a nightmare without a bank statement converter to convert PDF bank statements into XLS and CSV files.

Thanks to its proprietary AI model, it offers excellent accuracy and it's bank agnostic! You can try it for free up to 10 pages.